E-signature property conveyancing: a UK legal guide

E-signature property conveyancing is defined as the execution of legally binding property transaction documents through electronic means, without traditional wet-ink signatures. HM Land Registry began accepting electronic signatures meeting Practice Guide 82 criteria from 2020, marking a decisive shift in how UK property transactions are completed. Two signature types sit at the centre of compliant digital conveyancing: conveyancer-certified electronic signatures and Qualified Electronic Signatures (QES). Both carry legal weight, but each operates under distinct rules that buyers, sellers, and their solicitors must understand before a single document is signed.

The drive towards digital signing is not simply about convenience. Experts confirm the shift reduces administrative errors, accelerates completion, and strengthens security through verified identity checks. That combination of speed and compliance is why electronic conveyancing solutions are now mainstream rather than experimental.

What types of electronic signatures are legally accepted for property conveyancing in the UK?

The UK eIDAS framework defines three categories of electronic signature: simple, advanced, and qualified. Each carries a different level of evidentiary weight. Simple e-signatures cover typed names or scanned images of a signature. Advanced electronic signatures add identity verification and tamper-evidence. QES sits at the top, carrying the strongest legal presumption and requiring identity verification embedded directly into the signature process.

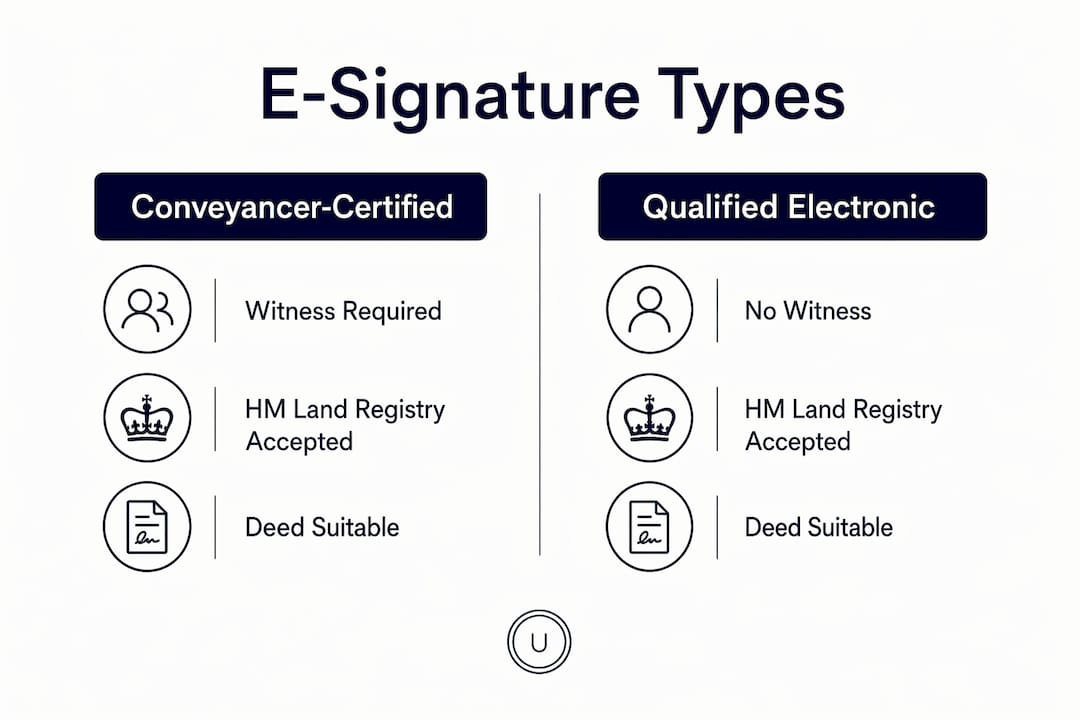

For property transaction e-signatures, HM Land Registry accepts two specific protocols.

Conveyancer-certified electronic signatures follow the Mercury approach, updated under Practice Guide 82. The signatory signs digitally while a witness is physically present. The conveyancer then certifies the process and submits the signed PDF deed alongside a certificate to Land Registry.

Qualified Electronic Signatures remove the witness requirement entirely. Identity is verified within the platform itself, making QES the more efficient route for straightforward transactions.

| Signature type | Witness required | Accepted by HM Land Registry | Suitable for deeds (e.g. TR1) |

|---|---|---|---|

| Simple e-signature | Yes (wet ink) | No | No |

| Advanced e-signature | Depends on protocol | Limited | No |

| Conveyancer-certified | Yes (physical presence) | Yes | Yes |

| Qualified (QES) | No | Yes (specific transactions) | Yes |

Lender adoption is accelerating. Nationwide Building Society now allows mortgage deeds to be signed using QES, following HM Land Registry’s confirmation of QES acceptance for specific transactions. That development signals a broader shift across the lending sector.

Pro Tip: Always confirm with your lender whether they accept QES before proceeding. Not every mortgage provider has updated its internal policies to match Land Registry acceptance.

How does the conveyancer-certified electronic signature process work?

The conveyancer controls every stage of the signing process. This is not a passive role. The conveyancer’s responsibilities include setting up and controlling the compliant signing platform, verifying identities, issuing one-time passwords (OTPs) to signatories and witnesses, and producing the certification that confirms compliance with Practice Guide 82 before documents go to Land Registry.

The process follows a defined sequence:

- Platform setup. The conveyancer selects a compliant platform and prepares the deed for digital execution.

- Identity verification. The conveyancer verifies the identity of the signatory and witness before any signing takes place.

- OTP issuance. One-time passwords are issued to both the signatory and the witness to authenticate their participation in the signing event.

- Physical witness presence. The witness must be physically present while the signatory applies their digital signature. Remote witnessing does not satisfy Practice Guide 82.

- Witness signs. The witness then applies their own electronic signature to confirm they observed the event.

- Conveyancer certification. The conveyancer produces a certificate confirming the process met all Practice Guide 82 requirements. This certificate must be in the individual conveyancer’s name, not the law firm’s name.

- Submission to Land Registry. The signed PDF deed and the certificate are submitted together to HM Land Registry.

The physical presence requirement catches many buyers and sellers off guard. A witness joining via video call does not meet the standard. The witness must be in the same room.

Common pitfalls include certification issued in the firm’s name rather than the individual conveyancer’s name, incomplete OTP records, and witnesses who signed remotely without realising the rules. Any of these errors can result in rejection by Land Registry and significant delays to completion.

Pro Tip: Ask your conveyancer to confirm in writing which platform they use and how they satisfy the physical witness requirement. A compliant firm will answer this without hesitation.

What are the benefits and challenges of using Qualified Electronic Signatures in conveyancing?

QES is defined as an electronic signature that embeds identity verification directly into the signing process, making the document tamper-evident from the moment it is signed. QES provides identity verification and ensures documents cannot be altered after signing, offering stronger security than traditional wet signatures.

The practical benefits for property buyers and sellers are significant:

- No physical witness required. The identity check built into QES replaces the need for a witness to be present, removing a common logistical obstacle.

- Reduced delays. Completion timelines shorten when parties do not need to coordinate physical signing events.

- Stronger audit trail. Every QES transaction generates a verifiable record of who signed, when, and on what platform.

- Lower error rates. Automated identity checks reduce the manual errors that slow down paper-based processes.

The limitations are equally worth knowing. HM Land Registry does not yet accept QES for every type of property document. Acceptance currently covers specific transaction types, and conveyancers must verify that the document in question falls within the approved scope. Not all lenders have adopted QES policies, so a transaction that qualifies at Land Registry level may still require a different approach to satisfy the mortgage lender.

Qualified Electronic Signatures eliminate the need for physical witnesses by embedding identity verification into the digital signature. However, conveyancers must still manage platform compliance and certification protocols rigorously. QES does not remove professional oversight. It changes where that oversight is applied.

Pro Tip: If your transaction involves a remortgage with a mainstream lender, ask specifically whether their mortgage deed template is approved for QES execution. Nationwide Building Society is confirmed; others vary.

What common misconceptions surround e-signatures in property conveyancing?

The most damaging misconception is that any electronic signature is sufficient for a property deed. Only QES or conveyancer-certified electronic signature protocols allow witness-free execution of deeds like TR1 forms. A standard e-signature applied through a general-purpose platform carries no legal weight for a land deed and will be rejected by HM Land Registry.

Several other misunderstandings regularly cause problems:

- “I signed electronically, so the deed is valid.” Signing electronically is only the first step. The conveyancer’s certification, the witness protocol, and the submission process must all be correct.

- “Any platform will do.” Platforms must meet the technical requirements set out in Practice Guide 82. A general document-signing tool does not automatically qualify.

- “Remote witnessing is acceptable.” Physical presence is a firm requirement for conveyancer-certified signatures. Video witnessing does not satisfy the standard.

- “Electronic signing of a contract is the same as signing a deed.” Contracts for the sale of property can be signed using a wider range of electronic methods. Deeds, including transfer forms and mortgage deeds, require the stricter protocols described above.

- “My conveyancer handles everything, so I do not need to understand the process.” Buyers and sellers who understand the requirements are better placed to spot errors and avoid delays.

The legal standing of an e-signature depends on intent, consent, attribution, and record retention. For deeds, those requirements are supplemented by the specific protocols in Practice Guide 82. Skipping any element puts the transaction at risk.

How can UK property buyers and sellers prepare for e-signature conveyancing?

Preparation reduces the risk of delays at the point of completion. The following steps apply whether you are buying, selling, or remortgaging.

- Verify your conveyancer’s platform. Ask which signing platform they use and confirm it meets Practice Guide 82 requirements. A compliant platform will have audit trail functionality, OTP issuance, and identity verification built in.

- Understand the witness rules. If your transaction uses conveyancer-certified electronic signatures, arrange for a witness who can be physically present at the signing event. The witness cannot be a party to the transaction.

- Access documents promptly. Electronic documents are time-sensitive. OTPs typically expire within a short window. Check your email and phone are accessible on the day of signing.

- Confirm lender acceptance. Before exchange, ask your solicitor to confirm that your mortgage lender accepts the signature method being used. This is particularly relevant for QES transactions.

- Retain copies and audit records. Request a copy of the signed deed and the conveyancer’s certificate for your own records. These documents form part of your property transaction audit trail and may be needed in future.

- Check Land Registry requirements for your specific document. TR1 transfer forms, mortgage deeds, and leases each have their own acceptance criteria. Do not assume that one document type covers all.

The legal requirements for electronic signatures in UK property transactions are updated periodically. Staying informed through your conveyancer and checking HM Land Registry guidance directly protects your position.

Pro Tip: Set a calendar reminder for the day of signing and keep your phone charged. Missing an OTP expiry window can delay completion by 24 hours or more.

Key takeaways

E-signature property conveyancing is legally valid in the UK only when the correct signature type and protocol are used, with conveyancer oversight and HM Land Registry compliance at every stage.

| Point | Details |

|---|---|

| Two accepted protocols | HM Land Registry accepts conveyancer-certified electronic signatures and Qualified Electronic Signatures for property deeds. |

| Physical witness still required | Conveyancer-certified signatures require the witness to be physically present, not remote. |

| QES removes witness requirement | Qualified Electronic Signatures embed identity verification, eliminating the need for a physical witness. |

| Lender acceptance varies | Confirm your mortgage lender’s policy before using QES; Nationwide Building Society is confirmed, others vary. |

| Certification must name the individual | The conveyancer’s certificate must be in the individual conveyancer’s name, not the firm’s, or Land Registry will reject it. |

Why the paper-to-digital shift in conveyancing is further along than most buyers realise

I have watched the conveyancing sector move from cautious experimentation with electronic signing to genuine operational reliance on it. What surprises me is how many buyers and sellers still arrive at completion with no idea that their deed was signed digitally. They assume paper is still the default. It is not, and that gap in awareness creates real risk.

The most consistent problem I see is not technology failure. It is process failure. A conveyancer uses a platform that technically qualifies, but the certification is issued in the firm’s name rather than the individual’s. Or a witness joins via video call because nobody explained the physical presence rule clearly enough. These are not edge cases. They are the errors that delay completions and, in some cases, require the entire signing process to be repeated.

My view is that QES will become the dominant method for residential conveyancing within the next few years. Nationwide Building Society’s adoption is a signal, not an outlier. When major lenders move, the rest of the market follows. The witness requirement for conveyancer-certified signatures has always been a logistical friction point, and QES removes it cleanly.

For buyers and sellers, the practical advice is straightforward. Ask your conveyancer which method they use, confirm it is compliant, and understand what you need to do on signing day. The technology is mature. The legal framework is settled. The only remaining variable is whether the people involved follow the process correctly.

— SignFlow Now

How SignFlow Now supports compliant e-signature conveyancing

Property transactions move fast, and a single process error can delay completion by days. SignFlow Now is built for exactly this environment.

SignFlow Now is fully aligned with HM Land Registry requirements and Practice Guide 82, providing conveyancer certification workflows, OTP-secured signing events, and complete document audit trails. The platform combines legally binding e-signatures with built-in AML screening and HMRC integration, so your conveyancing workflow stays compliant from client onboarding through to post-completion submission. Whether your firm handles conveyancer-certified signatures or QES transactions, SignFlow Now gives you the controls and the documentation to satisfy Land Registry at every stage. Explore the platform at signflownow.com.

FAQ

What is e-signature property conveyancing?

E-signature property conveyancing is the execution of legally binding property documents, including deeds and transfer forms, using electronic signatures rather than wet-ink signatures. HM Land Registry accepts this method under Practice Guide 82, provided the correct protocols are followed.

Are electronic signatures valid for property deeds in the UK?

Yes, but only when the correct type is used. Conveyancer-certified electronic signatures and Qualified Electronic Signatures are both accepted by HM Land Registry for deeds such as TR1 transfer forms. Standard e-signatures applied through general platforms are not sufficient.

Do I still need a witness for an electronic property deed?

It depends on the signature type. Conveyancer-certified electronic signatures require a witness to be physically present during the digital signing event. Qualified Electronic Signatures embed identity verification into the process and remove the witness requirement entirely.

Which lenders accept Qualified Electronic Signatures for mortgage deeds?

Nationwide Building Society confirmed QES acceptance for mortgage deeds following HM Land Registry’s approval of QES for specific transactions. Other lenders are adopting the approach at varying rates, so always confirm your lender’s current policy with your solicitor before proceeding.

What happens if the wrong e-signature type is used on a property deed?

HM Land Registry will reject the document. The signing process must be repeated using a compliant method, which can delay completion significantly. Using a compliant signing platform and a qualified conveyancer from the outset prevents this outcome.

Recommended

- Are Electronic Signatures Legally Binding in the UK? The Definitive Answer | SignFlow Now

- E-Signatures for US Real Estate Agents: ESIGN, UETA and What Realtors Need to Know | SignFlow Now

- Are Electronic Signatures Legal in the US? ESIGN vs UETA Explained | SignFlow Now

- Electronic Signatures in Australia: Corporations Act, State Law and What Businesses Need to Know | SignFlow Now