A suspicious transaction for an estate agent is any property deal that raises reasonable grounds to suspect money laundering or fraudulent activity, triggering a legal obligation to report it promptly to the relevant authorities. The industry term for this formal report is a Suspicious Activity Report, or SAR. Online real estate fraud losses exceeded $275 million in 2025, up from $173 million in 2024. That trajectory makes AML compliance a front-line business risk, not a back-office formality. Under regulations including the UK's Money Laundering Regulations 2017 (MLR 2017), the U.S. Bank Secrecy Act, AUSTRAC guidelines, and AMLD6 in the EU, estate agents carry direct legal responsibility for detecting and reporting suspicious activity.

What are the red flags of a suspicious transaction in property deals?

Recognizing a suspicious transaction early is the most effective defense against fraud liability. AUSTRAC's red flags list identifies several consistent patterns that agents should treat as immediate triggers for scrutiny.

The most common indicators include:

- Unexplained source of funds. A buyer cannot clearly explain where purchase funds originate, or the explanation changes across conversations.

- Urgency combined with document reluctance. The client pushes hard to close quickly but resists or delays providing standard identity or financial documents.

- Sudden changes in transaction instructions. Payment destinations, named parties, or deal structures shift without a clear commercial reason.

- Multiple rapid property transfers. Sales within 12–24 months of acquisition, especially at prices inconsistent with market values, can signal property flipping used to layer illicit funds.

- Cash payments or third-party accounts. Funds arriving from unrelated third parties or through unusual payment routes are a classic money laundering indicator.

- Mismatch between buyer profile and purchase value. A buyer whose stated income or business activity cannot plausibly support the transaction value warrants enhanced scrutiny.

- Unusual deposit or distribution instructions. Requests to hold deposits longer than necessary or to distribute profits to unrelated third parties are red flags for layering schemes.

Fraudsters now use AI-generated deepfakes and forged documents to impersonate sellers, with vacant land and absentee-owner properties being the most targeted asset types.

Pro Tip: Ask sellers an unexpected, property-specific question during a call, such as the name of a neighboring business or a detail about the property's history. A genuine owner answers easily. A fraudster using a script cannot.

What are the legal responsibilities of estate agents in reporting suspicious transactions?

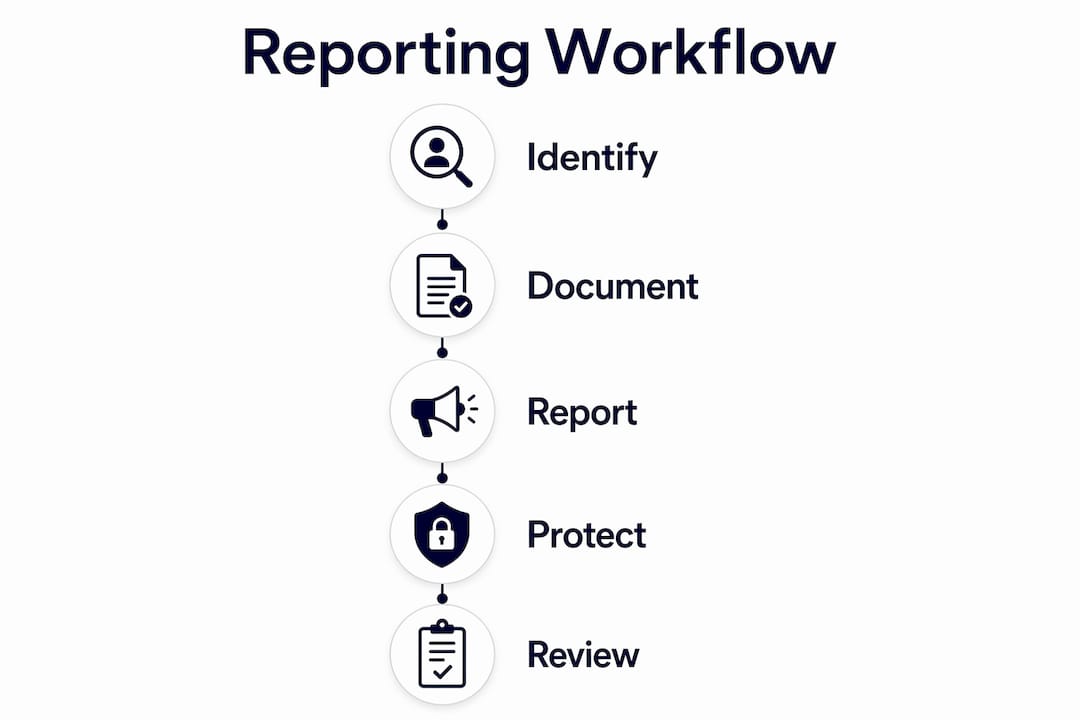

Estate agents do not need proof of wrongdoing to file a SAR. The legal threshold is reasonable grounds to suspect money laundering or fraud.

- Document your grounds for suspicion. Record the specific facts, behaviors, or inconsistencies that triggered concern.

- Escalate internally to your Money Laundering Reporting Officer (MLRO). If your firm has an MLRO, all suspicions must pass through that officer before external reporting.

- File a SAR with the relevant authority. In the UK, this goes to the National Crime Agency (NCA). In the U.S., reports go to FinCEN. In Australia, AUSTRAC receives them. In Canada, FINTRAC is the receiving body.

- Seek appropriate consent before proceeding. In the UK, agents must obtain a Defense Against Money Laundering (DAML) consent from the NCA before completing a transaction they have reported.

- Maintain confidentiality. Tipping off a client that a SAR has been filed is a criminal offense in most jurisdictions.

"Delays in making Suspicious Activity Reports violate anti-money laundering laws and can be prosecutable offenses, even if the transaction eventually fails to complete." — GOV.UK Estate Agency Discussion Notes

Agents who follow this sequence protect themselves legally and contribute to the broader effort to detect unusual activity in real estate before it causes wider harm.

Key Takeaways

| Point | Details |

|---|---|

| Reporting threshold | Reasonable suspicion suffices; agents do not need proof before filing a SAR. |

| Fraud losses are rising | Online real estate fraud exceeded $275 million in 2025, making vigilance a financial priority. |

| Timing is critical | Delaying a SAR submission creates criminal liability even if the transaction never completes. |

| Deepfakes are a real threat | AI-generated identity fraud now targets vacant land and absentee-owner properties most frequently. |

| Technology supports compliance | AML screening tools and multi-channel verification reduce manual risk and create documented audit trails. |

The compliance culture problem no one talks about

Real estate fraud has changed faster in the past two years than in the previous decade. The agents I speak with most often are not ignoring compliance. They are applying 2019 thinking to 2026 threats.

For agents looking to build that culture, e-signature compliance tools that integrate AML screening at the point of signing are the most practical starting point.

— SignFlow Now

SignFlow Now supports compliant real estate transactions

SignFlow Now combines legally binding e-signatures with built-in AML screening, sanctions checks, and client onboarding packs in a single platform. Agents receive real-time alerts on suspicious client activity and meet requirements under MLR 2017, AUSTRAC, FINTRAC, and AMLD6. The platform supports team-level compliance management for agencies operating across multiple offices or jurisdictions.

FAQ

What is a suspicious transaction in real estate?

A suspicious transaction is any property deal that gives an estate agent reasonable grounds to suspect money laundering or fraud. No proof is required; reasonable suspicion based on observable facts is the legal threshold.

When must an estate agent file a SAR?

An agent must file a Suspicious Activity Report as soon as reasonable grounds for suspicion arise. Delaying submission creates criminal liability under AML laws, even if the transaction does not complete.

What are the most common red flags in property deals?

The most common indicators include unexplained sources of funds, urgency combined with document reluctance, sudden changes in payment instructions, rapid multiple property transfers, and a mismatch between the buyer's profile and the purchase value.

Does reporting a suspicious transaction harm the client relationship?

Agents who report in good faith receive legal protection from civil liability. Confidentiality rules prevent disclosure to the client, so the filing does not automatically damage the relationship.

How does AI fraud affect estate agent compliance?

Fraudsters now use AI-generated deepfakes and forged documents to impersonate sellers, particularly in vacant land transactions. Agents must verify identity through live video calls and independent phone contact, not email or document copies alone.