Electronic signature realtor legality: 2026 compliance guide

Electronic signatures are legally binding for the vast majority of real estate contracts in the United States under the federal Electronic Signatures in Global and National Commerce Act (ESIGN Act) and the Uniform Electronic Transactions Act (UETA). For realtors, understanding electronic signature realtor legality is no longer optional. Regulatory scrutiny has intensified in 2026, with new anti-money laundering obligations sitting alongside established signature laws. This guide sets out which documents qualify, what the law requires to make a signature enforceable, and where compliance gaps most commonly arise in practice.

Which real estate documents can use electronic signatures?

Electronic signatures are legally binding for the majority of documents realtors handle daily. The following categories are well-established as e-signable under ESIGN and UETA:

- Listing agreements between sellers and agents

- Buyer representation contracts

- Purchase and sale agreements

- Lease agreements and rental applications

- Disclosure forms and addenda

- Offer letters and counter-offers

The exceptions matter considerably. Certain documents still require wet-ink signatures or Remote Online Notarisation (RON): deeds, wills, and instruments that must be recorded with a county recorder office. Improperly executed deeds risk creating a “cloud on title,” which is a defect in the chain of ownership that can trigger costly legal disputes and delay or void a sale entirely.

Many county recorder offices retain legacy requirements for wet-ink signatures and notarisation on deeds, even where electronic advances have otherwise modernised the process. Local recorders may reject electronic recordings if these requirements are not met, making early consultation with the relevant authority a practical necessity rather than an optional step.

Pro Tip: Before any transaction involving a deed or recordable instrument, contact the county recorder’s office directly to confirm their current requirements. Do not assume that because a platform supports e-signatures, the recorder will accept them.

How do ESIGN and UETA establish the validity of electronic signatures?

The ESIGN Act and UETA share four foundational pillars that determine whether an electronic signature is enforceable in a real estate context:

- Intent to sign. The signer must take a deliberate action, such as clicking “I agree” or drawing a signature, that demonstrates they intended to execute the document.

- Consent. All parties must consent to conduct the transaction electronically. This consent must be documented and, in consumer transactions, must meet specific disclosure requirements under ESIGN.

- Attribution. The signature must be linked to the specific person who signed. Platforms achieve this through login credentials, email verification, and unique signing links.

- Record retention. Signed documents must be stored in a format that can be accurately reproduced and accessed later by all parties.

Audit trails are the technical mechanism that satisfies attribution and retention simultaneously. Audit trails with IP addresses, timestamps, and document version linkage are essential to satisfy these requirements. A platform that stores only the signed PDF without capturing the signing event metadata provides a document that is far harder to defend if challenged in court or during a regulatory investigation.

State law adds a further layer of complexity. UETA has been adopted in 47 states, but each state may apply it with minor variations. Illinois, New York, and Washington enacted their own electronic signature statutes before UETA, which means realtors operating across state lines must verify which framework governs each transaction. The interaction between state law and local recorder requirements is where most enforceability problems originate.

| Requirement | What it means in practice | How platforms address it |

|---|---|---|

| Intent to sign | Deliberate signing action by the party | Click-to-sign, drawn signature, or typed name |

| Consent | Agreement to transact electronically | Consent disclosure at session start |

| Attribution | Linking signature to the individual | Email verification, unique signing link, IP capture |

| Record retention | Accessible, reproducible signed record | Tamper-evident storage with full audit log |

What compliance risks do realtors face beyond signature validity?

Signature legality is only one part of the compliance picture. Digital closings require integrated compliance workflows covering identity verification, AML screening, and secure document storage. Treating an e-signature platform as a standalone tool, rather than part of a broader compliance process, is one of the most common realtor e-signature compliance gaps in practice.

The 2026 FinCEN Residential Real Estate Rule has raised the stakes considerably. Penalties for AML breaches can exceed $250,000 and include custodial sentences. Data privacy violations carry fines of up to $7,500 per incident. These figures make the cost of non-compliance far exceed the cost of building a proper compliance workflow from the outset.

Real estate agents are classified as obliged entities under AML frameworks. E-signatures are one checkpoint in AML and counter-financing of terrorism (CFT) compliance, not a substitute for it. The following are the most common examples of realtor compliance breaches in 2026:

- Failing to conduct beneficial ownership checks on corporate buyers

- Accepting third-party payments without verifying the source of funds

- Using e-signature platforms that do not integrate with identity verification tools

- Storing signed documents in isolated silos that cannot be retrieved during a regulatory audit

- Neglecting to update client due diligence records when transaction details change

E-signature platforms storing documents in silos often fail regulatory investigation requirements. A signed purchase agreement held in one system, with identity verification records in another and AML screening results in a third, creates a fragmented audit trail that regulators will treat as a compliance failure regardless of whether each individual step was completed correctly.

Pro Tip: Map your entire transaction workflow before selecting an e-signature platform. Identify every compliance checkpoint, from initial identity verification through to document storage, and confirm that your chosen platform either covers each step or integrates directly with tools that do.

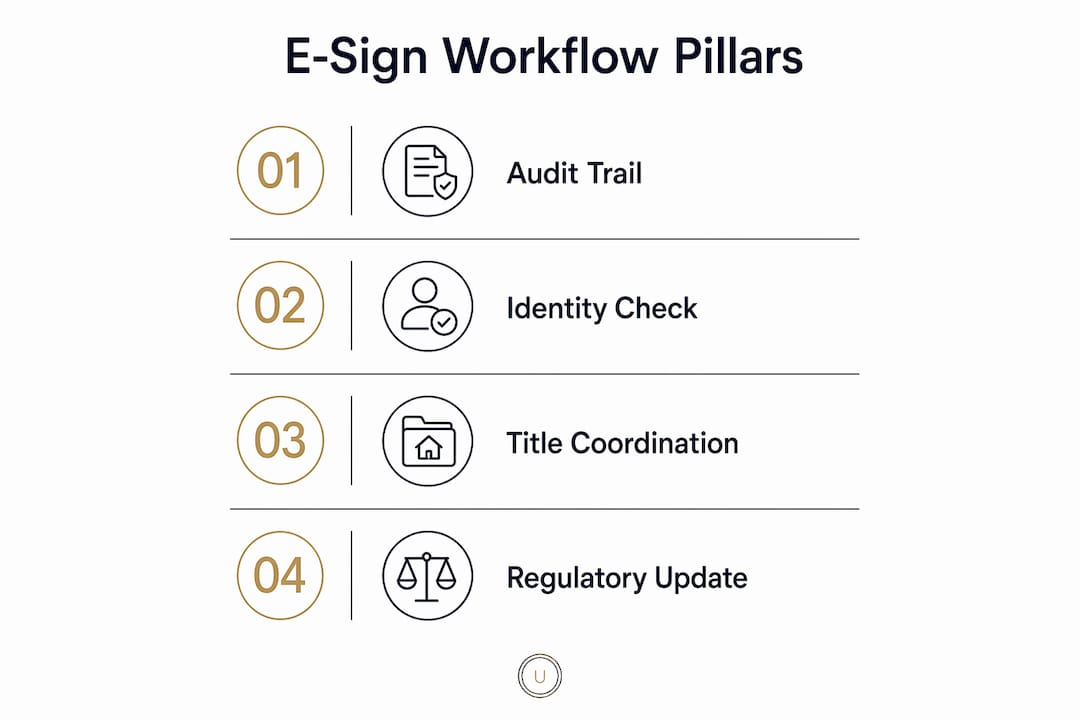

How should realtors build a legally compliant e-signature workflow?

A compliant e-signature workflow for real estate professionals rests on four operational pillars. Each addresses a distinct type of real estate compliance risk and, together, they form a defensible process that withstands both contractual challenge and regulatory scrutiny.

Audit trail integrity

Every signing event must capture the signer’s IP address, the precise timestamp, and a cryptographic link to the specific version of the document signed. If a document is amended after signing, the audit trail must record that amendment separately. Platforms that do not support document version linkage create a gap that opposing counsel or a regulator can exploit.

Identity verification at the point of signing

Identity verification must occur before the signature is captured, not as a separate onboarding step days earlier. Acceptable methods include government-issued ID checks, biometric verification, and knowledge-based authentication. The verification record must be stored alongside the signed document so that both can be produced together during an investigation.

Coordination with title companies and notaries

For transactions involving deeds or other recordable instruments, realtors must coordinate with title companies and notaries before the signing event. Remote Online Notarisation is now available in the majority of US states, but the notary must use a platform approved by the relevant state authority. Confirm RON eligibility with your title company at the outset of each transaction.

Regulatory monitoring and continuing education

AML rules, state electronic signature statutes, and county recorder requirements all change. Realtors should subscribe to updates from FinCEN, their state real estate commission, and the National Association of Realtors. Building a quarterly review of compliance requirements into your practice calendar prevents the gradual drift that turns minor gaps into material breaches. For a detailed overview of AML reporting obligations specific to real estate agents in 2026, the regulatory landscape has shifted significantly since 2024.

Key takeaways

Electronic signatures are legally valid for most real estate contracts under ESIGN and UETA, but compliance requires audit trails, identity verification, and integrated AML workflows, not just a signed document.

| Point | Details |

|---|---|

| Legal foundation | ESIGN and UETA make e-signatures enforceable when intent, consent, attribution, and retention are all satisfied. |

| Document exceptions | Deeds and recordable instruments still require wet-ink signatures or RON; improperly executed deeds risk a cloud on title. |

| Audit trail requirements | Platforms must capture IP addresses, timestamps, and document version linkage to satisfy attribution and retention rules. |

| AML obligations | Realtors are obliged entities under AML frameworks; e-signatures are one compliance checkpoint, not a complete process. |

| Integrated workflows | Siloed e-signature platforms fail regulatory audits; identity verification and AML screening must connect to document storage. |

Why I think most realtors are still underestimating the compliance shift

I have spent considerable time working with real estate professionals across the US and UK, and the pattern I see most consistently is this: realtors adopt e-signatures to save time, which is entirely reasonable, but they stop there. They treat the signed PDF as the end of the compliance obligation rather than the beginning of an audit-ready record.

The 2026 FinCEN Residential Real Estate Rule has changed the calculus entirely. The question regulators now ask is not simply “was the document signed?” but “can you demonstrate, with a complete and connected audit trail, who signed it, when, after what identity checks, and in the context of what AML screening?” A realtor who cannot answer all of those questions from a single, integrated record is exposed, regardless of whether the signature itself is technically valid.

Contract precision matters as much as signature validity. Legal challenges in real estate transactions arise far more often from ambiguous contract terms than from disputed signatures. I have seen transactions unravel not because the e-signature was challenged, but because the underlying document contained contradictory clauses that the parties had not read carefully before clicking to sign. The speed that e-signatures enable can, paradoxically, increase the risk of documentation errors if realtors do not build in a review step before sending.

My practical advice is to treat your e-signature platform as one component in a compliance system, not as the system itself. Evaluate it against the full workflow: identity verification, AML screening, beneficial ownership checks, document storage, and audit log retrieval. If any of those steps sits outside the platform with no direct integration, you have a gap that will cost you more to fix after a regulatory inquiry than before one.

— SignFlow Now

SignFlow Now: built for realtors who need more than a signature

Realtors operating in 2026 need a platform that goes beyond capturing a signature and closing the document. SignFlow Now is built for exactly that requirement.

SignFlow Now combines legally binding e-signatures for realtors with built-in AML screening, identity verification, and tamper-evident audit trails, all within a single workflow. Every signing event captures the IP address, timestamp, and document version linkage required under ESIGN and UETA. Signed documents are stored in a format that can be retrieved and presented during a regulatory audit without manual assembly from multiple systems. For realtors who need a fully integrated compliance platform, SignFlow Now covers the complete transaction record from client onboarding through to signed document storage.

FAQ

Are electronic signatures legally valid for real estate contracts?

Electronic signatures are legally binding for most real estate contracts in the US under the ESIGN Act and UETA, provided the signing process satisfies intent, consent, attribution, and record retention requirements.

Which real estate documents still require wet-ink signatures?

Deeds, wills, and instruments requiring recording with a county recorder office typically still require wet-ink signatures or Remote Online Notarisation. Improperly executed deeds can create a cloud on title and trigger costly legal disputes.

What is required for an electronic signature audit trail to be enforceable?

A defensible audit trail must capture the signer’s IP address, a precise timestamp, and a cryptographic link to the specific document version signed. Platforms that store only the signed PDF without this event metadata are significantly harder to defend in court.

How do AML obligations affect realtors using electronic signatures?

Real estate agents are obliged entities under AML frameworks, including the 2026 FinCEN Residential Real Estate Rule. Electronic signatures are one compliance checkpoint within a broader AML process that must also include identity verification, beneficial ownership checks, and secure document storage.

What are the most common e-signature compliance gaps for realtors?

The most common gaps include using platforms that do not integrate identity verification with document storage, failing to conduct beneficial ownership checks on corporate buyers, and storing signed documents in isolated systems that cannot produce a connected audit trail during a regulatory investigation.

Recommended

- E-Signatures for US Real Estate Agents: ESIGN, UETA and What Realtors Need to Know | SignFlow Now

- E-Signature Property Conveyancing: A UK Legal Guide | SignFlow Now

- Electronic Signatures in Canada: Federal Law, PIPEDA and Provincial Variations | SignFlow Now

- Suspicious Transaction Estate Agent: 2026 Compliance Guide | SignFlow Now