Property sale AML screening: your 2026 compliance guide

Property sale AML screening is the process by which real estate professionals verify client identities, assess financial risk, and screen buyers and sellers against sanctions lists to prevent money laundering through property transactions. The formal industry term is Customer Due Diligence, or CDD, and it sits at the heart of anti-money laundering compliance for every regulated property sale. Real estate is a prime target for financial crime because high-value transactions, long ownership periods, and complex funding structures make it easy to conceal illicit funds. Regulators including AUSTRAC, FinCEN, and HMRC have each tightened their requirements in 2026, making it critical that agents and conveyancers understand exactly what property sale due diligence demands of them.

What are the core components of property sale AML screening?

AML screening in a property transaction is not a single check. It is a structured sequence of verifications that must be completed before you provide any designated service to a client.

The mandatory components are:

- Identity verification. Collect and verify government-issued photo ID and proof of address for every buyer and seller. For companies or trusts, you must identify the ultimate beneficial owner (UBO), the natural person who ultimately controls or benefits from the entity.

- Know Your Customer (KYC) procedures. Gather information about the client’s occupation, the nature of the transaction, and their relationship to the property. KYC in property sales goes beyond a passport check; it builds a risk profile for each party.

- Source of funds and source of wealth checks. Ask clients to document where the purchase funds originate. Bank statements, mortgage offers, inheritance records, and sale proceeds from a prior property are all acceptable evidence. Unexplained cash or funds routed through multiple accounts require further scrutiny.

- Sanctions and PEP screening. Screen every client against consolidated sanctions lists and identify Politically Exposed Persons before providing any service. A PEP is not automatically disqualified, but the relationship requires enhanced due diligence.

- Ongoing monitoring. CDD is not a one-time event. If a transaction changes materially, for example the buyer switches from a personal purchase to a company purchase, you must re-screen.

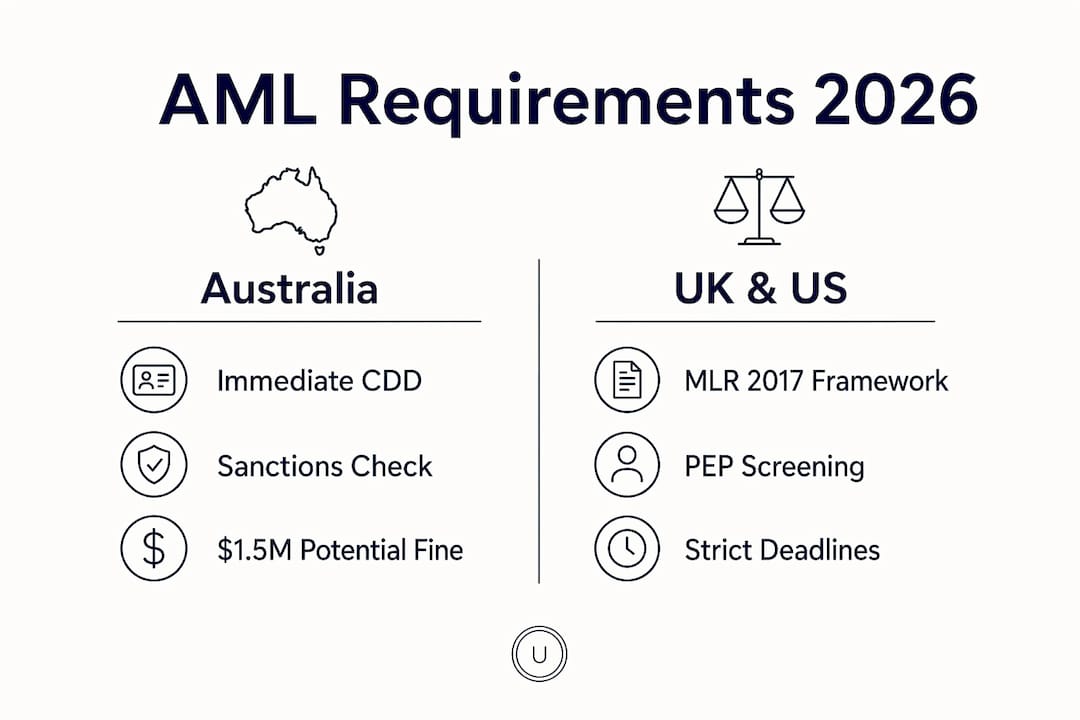

The timing of these checks matters. Australian agents must complete CDD immediately after signing the Sales Authority Agreement and before marketing the property, starting 1 july 2026. Conducting checks after you have already invested time in a transaction creates pressure to overlook red flags.

Pro Tip: Frame CDD as a standard intake procedure, not a special investigation. Clients accept identity checks far more readily when they are presented as a routine step that every client completes, rather than a sign of suspicion.

How do AML requirements differ by jurisdiction in 2026?

The obligations are consistent in principle but differ significantly in detail and deadline across Australia, the UK, and the US. The table below summarises the key differences.

| Jurisdiction | Regulatory framework | Key 2026 change | Penalty for non-compliance |

|---|---|---|---|

| Australia | AUSTRAC Tranche 2 AML/CTF Act | Seven AML obligations apply from 1 july 2026, including enrolment, CDD, sanctions screening, and staff training | Fines, suspension, and criminal prosecution |

| United States | FinCEN Real Estate Geographic Targeting Order (GTO) | Non-financed residential transfers to entities must be reported by the month following closing or 30 days after closing, effective march 2026 | Negligent violations up to $1,430 per violation; wilful violations up to $71,545 or the transaction value, plus possible imprisonment |

| United Kingdom | Money Laundering Regulations 2017 (MLR 2017) | Ongoing obligation to screen against UK sanctions lists and conduct enhanced due diligence for high-risk clients | Fines, loss of authorisation, and criminal liability |

| European Union | AMLD6 and incoming AMLR | Complex ownership structures and cross-border flows require improved due diligence and UBO identification | Administrative sanctions and reputational consequences |

The US penalties are particularly instructive. A negligent violation costs up to $1,430 per instance. That figure compounds quickly across a busy agency. Wilful non-compliance carries penalties up to $71,545 or the full transaction value, whichever is greater, plus the possibility of imprisonment. These are not theoretical risks; failure to screen exposes agents and vendors to fines, suspension, and reputational damage that can end a practice.

For UK agents, MLR 2017 remains the primary framework. You must conduct CDD on every client, screen against the UK Consolidated Sanctions List, and apply enhanced due diligence where a client or transaction presents higher risk. HMRC is the supervisory authority for most estate agents in England and Wales, and it conducts compliance visits.

What are the red flags in property transactions?

Red flags in property transactions fall into three categories: behavioural, transactional, and documentary. Recognising all three is the difference between a compliant practice and one that unknowingly facilitates financial crime.

Behavioural red flags are often the earliest warning signs. Client behavioural cues such as nervousness, refusal to disclose the source of wealth, and frequent changes to payment instructions are as important as document verification in identifying suspicious activity early. A client who cannot explain where their funds come from, or who becomes hostile when asked, warrants a Suspicious Activity Report (SAR) regardless of how straightforward the property itself appears.

Transactional red flags include:

- Purchases significantly above or below market value without a clear commercial reason.

- Rapid property flipping, particularly where the resale price bears no relation to any improvement works.

- Funds arriving from multiple third parties or from jurisdictions with weak AML controls.

- Payment by cryptocurrency or other virtual assets without a clear audit trail.

- Last-minute changes to the buyer’s identity or ownership structure.

Documentary red flags centre on the ownership structure. Complex ownership structures, cross-border flows, and anonymity are the EU’s stated primary concerns under AMLD6. Tracing UBOs requires looking past company documents to uncover hidden owners through multiple corporate layers. A purchase made through a chain of offshore entities, where no natural person is readily identifiable, is a significant red flag.

Pro Tip: When you identify a potential red flag, document your reasoning in writing before you decide whether to proceed or file a SAR. A clear contemporaneous record protects you if the matter is later reviewed by a regulator or court.

Real estate is targeted by money launderers precisely because high-value transactions, long ownership periods, and opaque funding sources make it easier to conceal illicit funds than in most other asset classes. Regulators expect a risk-based approach that prioritises UBO identification and sanctions screening above all else.

How to implement AML screening without disrupting client relationships

Effective AML compliance does not require you to treat every client as a suspect. The key is to embed checks into your standard onboarding workflow so that they feel routine rather than intrusive.

- Build CDD into your client care letter. Send identity verification requests and source of funds questionnaires alongside your terms of engagement. Clients who receive these documents before the first meeting understand that compliance is a condition of the service, not a reaction to something they have done.

- Use AML screening software to automate sanctions and PEP checks. Manual searches against sanctions lists are slow and prone to error. Automated platforms run checks in seconds and generate an auditable record. SignFlow Now combines built-in AML screening with e-signature collection, so identity verification and document signing happen in a single workflow.

- Communicate the legal basis clearly. Clear communication about AML screening’s legal necessity reassures clients and helps maintain professional relationships during otherwise sensitive procedures. Tell clients that the checks are a legal requirement under MLR 2017, AUSTRAC, or FinCEN rules as applicable, not a matter of personal discretion.

- Retain all records for at least 7 years. Record retention and staff training are statutory requirements. Store CDD documents, screening results, and any SAR decisions in a secure, retrievable system. Seven years is the minimum; some jurisdictions require longer.

- Train your team annually. Staff who cannot recognise a red flag are a compliance liability. Annual training on AML obligations, red flag indicators, and SAR procedures is a regulatory requirement under AUSTRAC’s Tranche 2 framework and is best practice under MLR 2017. For agents handling suspicious transactions, documented training records also provide a degree of regulatory protection.

Automating AML screening and embedding it as a routine part of the sales process improves both compliance and client acceptance. Framing checks as regulatory requirements, rather than discretionary investigations, reduces friction and improves the quality of the data you collect for risk assessments.

Key takeaways

Property sale AML screening requires identity verification, sanctions and PEP screening, source of funds checks, UBO identification, and 7-year record retention as non-negotiable compliance obligations across all major jurisdictions.

| Point | Details |

|---|---|

| CDD must happen early | Complete identity and sanctions checks before marketing the property, not after offers are received. |

| Jurisdictional rules differ | Australia, the UK, the US, and the EU each have distinct frameworks and 2026 deadlines with serious penalties for non-compliance. |

| Behavioural red flags matter | Nervousness, refusal to disclose wealth sources, and payment instruction changes are as significant as document irregularities. |

| UBO identification is mandatory | To Look past company documents to identify the natural person who ultimately controls or benefits from the transaction. |

| Retain records for 7 years | All CDD documents, screening results, and SAR decisions must be stored securely and remain retrievable for at least 7 years. |

Why normalising AML screening is the real compliance challenge

The technical requirements of AML screening are well-documented. The harder problem is cultural. In my experience working with estate agents and conveyancers, the biggest compliance failures do not come from ignorance of the rules. They come from agents who know the rules but feel uncomfortable applying them to clients they have known for years, or to high-value buyers who project confidence and impatience.

The uncomfortable truth is that money launderers rely on exactly that discomfort. They choose professional, well-presented representatives. They move quickly and create time pressure. They make you feel that asking for source of funds documentation is an insult.

The solution is not to become suspicious of everyone. It is to make the process so routine that no individual client can feel singled out. When every client receives the same onboarding pack, the same identity verification request, and the same source of funds questionnaire, the process loses its personal edge. I have seen practices reduce client pushback dramatically simply by sending CDD requests before the first meeting, as part of the initial engagement letter, rather than raising them mid-transaction.

The other area where I see consistent gaps is UBO identification for company buyers. Agents often accept a certificate of incorporation and stop there. Tracing beneficial ownership through multiple corporate layers is genuinely difficult, but it is also where the highest-risk transactions hide. If you cannot identify a natural person who controls more than 25% of the purchasing entity, that is not a paperwork inconvenience. It is a red flag that requires escalation.

Staying current with regulatory changes is also non-negotiable. The 2026 updates from AUSTRAC, FinCEN, and the EU represent the most significant tightening of real estate AML obligations in a decade. Agents who treat compliance as a one-time setup rather than an ongoing practice will find themselves on the wrong side of a regulatory visit.

— SignFlow Now

SignFlow Now for property sale AML compliance

Real estate professionals who need to meet their AML obligations without adding administrative burden to every transaction will find SignFlow Now built for exactly that purpose.

SignFlow Now combines built-in AML screening with legally binding e-signatures, so identity verification, sanctions screening, and document execution happen within a single client onboarding workflow. There is no need to manage separate systems for KYC checks and contract signing. The platform is compliant with MLR 2017, AUSTRAC, FINTRAC, and AMLD6, making it suitable for agents operating across the UK, Australia, the US, Canada, and the EU. You can collect client documents, run PEP and sanctions checks, and obtain signatures on your Sales Authority Agreement in one place. Visit SignFlow Now to see how the platform supports your compliance obligations from the first client contact through to completion.

FAQ

What is AML screening in a property sale?

AML screening in a property sale is the process of verifying client identities, checking them against sanctions and PEP lists, and assessing the source of their funds before completing the transaction. It is a legal requirement under frameworks including MLR 2017, AUSTRAC, and FinCEN rules.

When must AML checks be completed in a property transaction?

AML checks must be completed before you provide any designated service to the client. Under AUSTRAC’s Tranche 2 rules effective from 1 july 2026, Australian agents must complete CDD immediately after signing the Sales Authority Agreement and before marketing the property.

What happens if an estate agent fails to conduct AML screening?

Penalties range from fines and suspension to criminal prosecution. In the US, wilful violations of FinCEN reporting rules carry penalties up to $71,545 or the full transaction value, plus possible imprisonment. UK agents risk fines and loss of authorisation under MLR 2017.

What is a Politically Exposed Person (PEP) in property transactions?

A PEP is an individual who holds or has held a prominent public position, such as a government minister or senior official, and whose financial dealings carry a higher risk of corruption. Identifying a PEP does not prevent a transaction but requires enhanced due diligence before proceeding.

How long must AML records be kept after a property sale?

AML records must be retained for a minimum of 7 years after the end of the business relationship or transaction. This includes identity documents, screening results, source of funds evidence, and any SAR decisions made during the process.